Genesis Financial and Interactive Brokers is a full-featured investment platform built for all investors. It offers a wealth of assets and data, and users can trade equities, ETFs, mutual funds, bonds, options, futures, foreign currency, and more in both the U.S. and scores of foreign markets.

Interactive Brokers and Genesis offers a comprehensive set of asset classes. This includes equities, ETFs, mutual funds, bonds, options, futures, foreign currency, cryptocurrency, REITs, certificates of deposit, treasuries, money market and more. Depending on availability and legal restrictions, you can trade these assets not only on U.S. markets but on more than 100 different markets worldwide. Over $10,000 in Cash can return rates equivalent to many bank accounts and will increase or decrease according to federal funds rate changes.

In addition to its Trader Workstation, Interactive Brokers and Genesis also offers a web-based an app-based version of its trading platform. These portals give you access to the same trading network (as opposed to many other companies which set up multiple different products around assets and devices). The web and app-based versions of Genesis -Interactive Brokers offer many of the same features as its core brand, however, unlike many online trading platforms they are not the firm’s flagship product.

Finally, as a niche but noteworthy feature, Genesis Interactive Brokers has jumped on the movement toward socially conscious investing with its Impact Dashboard. This tool helps you sort assets and build investment strategies around different social priorities such as environmental concerns, social justice issues and political representation.

There are many different types of investment vehicles available to investors, including savings accounts, money market accounts, stocks, bonds, mutual funds, ETFs, precious metals, derivatives, American Depositary Receipts, limited partnership interests, shares of beneficial interest, tracking stocks, convertible debentures, preferred stocks, rights, and warrants. Each of these investment vehicles has its own unique characteristics and benefits, and understanding them is important for informed investing.

The Rule of 72 is a quick, useful formula that is popularly used to estimate the number of years required to double the invested money at a given annual rate of return. Alternatively, it can compute the annual rate of compounded return from an investment given how many years it will take to double the investment. The Rule of 72 applies to compounded interest rates and is reasonably accurate for interest rates that fall in the range of 6% and 10%. The Rule of 72 can be leveraged in two different ways to determine an expected doubling period or required rate of return. For different situations.

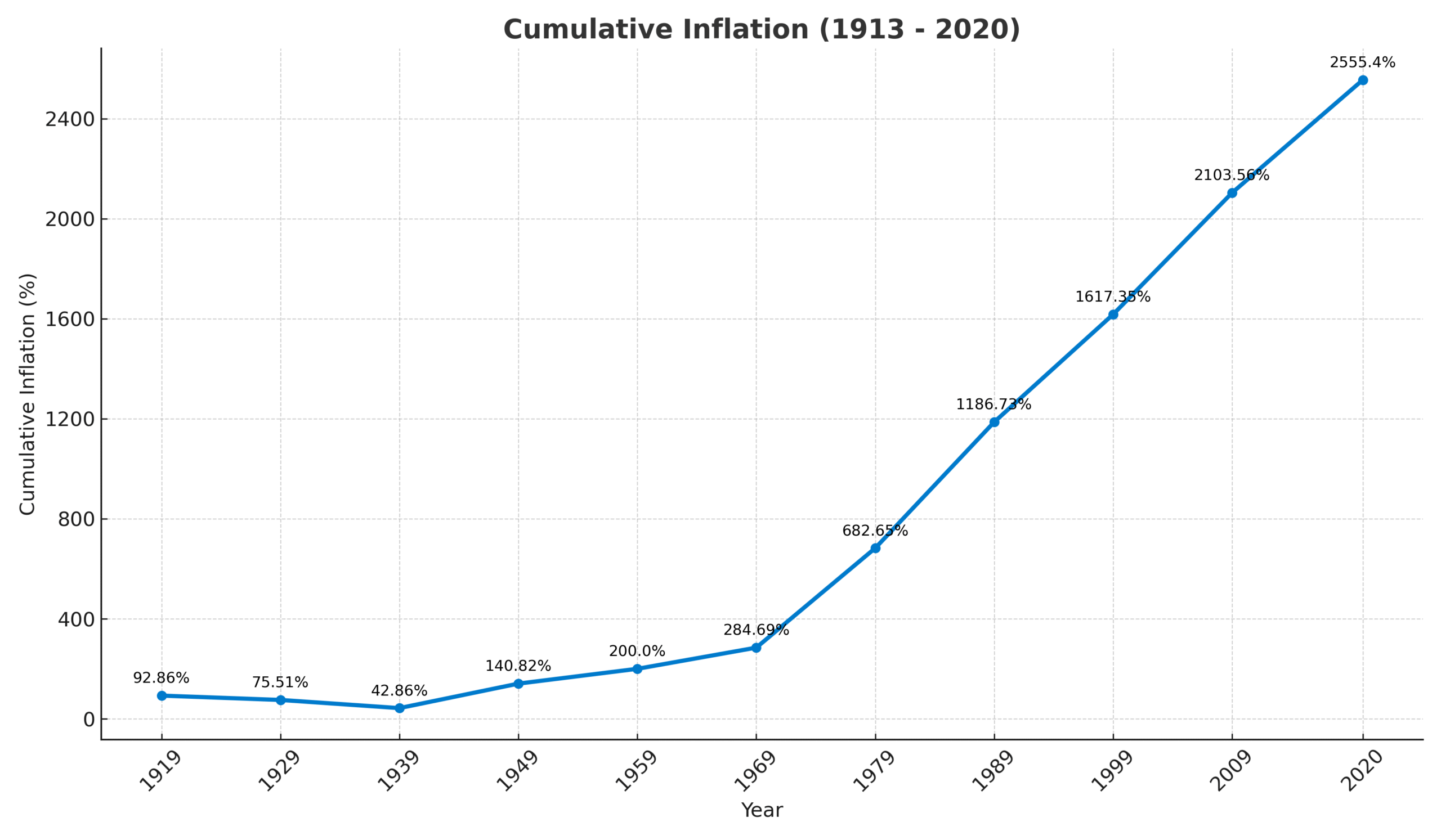

The chart below shows the average annual inflation rate for each decade since 1913. The average annual inflation rate since 1913 is 3.10%. This rate of inflation has resulted in prices increasing by 2555% since 1913. This means that something that cost $100 in 1913 would cost $2,555.

Investing with an competent investment advisor will grow your assets at 10 % a year – If you take out inflation @ 3.10 % that would be and average of 6.90% per year – That would double your money in around 10 years . In other words $10,000 would increase 100% to $20,000 – That is real spending power BEATS INFLATION.

Retirement planning is the process of planning for one’s retirement, including saving and investing for retirement, estimating future expenses and income, and planning for other retirement-related goals. It is important to plan for retirement early in life, as it can help ensure that one has enough money to live comfortably during retirement.

An IRA (Individual Retirement Account) is a type of savings account that provides tax benefits for retirement savings in the United States. There are two main types of IRAs: Traditional and Roth. Contributions to a Traditional IRA may be tax-deductible, and the money grows tax-deferred, but withdrawals in retirement are taxed as income. Contributions to a Roth IRA are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. IRAs have contribution limits and restrictions on withdrawals before age 59 1/2 to encourage long-term savings for retirement.

For tax year 2025, the total you can contribute to all your IRAs (Traditional + Roth) is $7,000, or $8,000 if you’re age 50 or older (includes the $1,000 catch-up). Income limits can affect Roth IRA eligibility and whether Traditional IRA contributions are deductible. For 2025, Roth IRA full contributions are allowed if MAGI is under $150,000 (single/HOH) or under $236,000 (married filing jointly), with phase-outs at $150,000–$165,000 and $236,000–$246,000, respectively. Traditional IRA deduction phase-outs (when covered by a workplace plan) are $79,000–$89,000 (single/HOH) and $126,000–$146,000 (MFJ for the covered spouse); if you’re not covered but your spouse is, the MFJ phase-out is $236,000–$246,000. Married filing separately phase-outs remain $0–$10,000. IRS

2026 IRA limits haven’t been announced as of August 25, 2025; the IRS typically releases next-year retirement limits in October–November. Milliman

As always, specific deductibility and Roth eligibility depend on your filing status and income—consult your tax professional for personalized advice.

It’s important to note that there are contribution limits and eligibility requirements for IRAs, so make sure to research and understand these before you start the funding process.

You can take money from an IRA at any time. If you’re under age 59½, most withdrawals are taxable and also hit with a 10% early-distribution penalty. A higher 25% penalty applies to SIMPLE IRAs if you withdraw within the first two years of participating in the plan. Exceptions can waive the penalty (but not ordinary income tax) for situations such as death, disability, unreimbursed medical expenses above 7.5% of AGI, health-insurance premiums while unemployed (IRA only), higher-education expenses (IRA only), a first-time home purchase up to $10,000 (IRA only), IRS levy, substantially equal periodic payments (72(t)), qualified disaster relief (up to $22,000), domestic-abuse distributions (lesser of $10,000 or 50% of the account), and $1,000 “emergency personal expense” distributions (with repayment/limitations). If an exception applies but your 1099-R doesn’t show it, you can claim it on Form 5329. IRS

New for this period: effective 2024, the IRS finalized guidance for the $1,000 emergency and domestic-abusepenalty exceptions noted above. Effective late 2025/2026, SECURE 2.0 §334 allows penalty-free distributions of up to $2,500 per year from retirement accounts (including IRAs) to pay premiums for certain certified long-term-care insurance (taxes may still apply); details are being implemented by Treasury/IRS. IRSGroom Law GroupThe Tax Adviser

Special Roth IRA note: your regular Roth contributions (basis) can be withdrawn anytime tax- and penalty-free. Earnings are tax-/penalty-free only when the withdrawal is a qualified distribution (the 5-year rule plus an event like age 59½, death, disability, or first-home up to $10,000). Amounts converted to Roth generally have their own 5-year clock for the 10% penalty if taken before 59½. See the IRS ordering rules in Pub. 590-B. IRS

Rules can be nuanced (plan vs. IRA differences, state tax, documentation). For specific planning and to minimize taxes/penalties, consider consulting your tax professional. IRS

It is difficult to determine the exact amount you will earn in an IRA if it grows at 7% per year for 25 years, as it depends on the starting balance and contributions made over the 25-year period. However, you can use the formula for compound interest to estimate the future value of your IRA. The formula is:

FV = PV * (1 + r/n)^(nt)

Where:

PV = the present value or starting balance of the IRA r = the annual interest rate (7%) n = the number of times the interest is compounded per year t = the number of years (25)

Note that this is just an estimate and actual results may differ due to various factors such as taxes, fees, and inflation.

To calculate the total amount you would have in an IRA after 25 years with an annual contribution of $6,500 and a 7% interest rate, you can use the formula:

A = P * (1 + r/n)^(nt)

Where: A is the end amount P is the principal amount (the amount you initially invest) r is the interest rate (expressed as a decimal) n is the number of times interest is compounded per year t is the number of years

In this case: P = 6500 * 25 = $162,500 (total contribution over 25 years) r = 0.07 n = 1 (once per year) t = 25

Plugging these values into the formula, you get:

A = $162,500 * (1 + 0.07/1)^(1 * 25) = $657,914.07

So, after 25 years of contributing $6,500 annually and with a 7% interest rate, you would have approximately $657,914.07.

The IRA Match generally would be taxable during a conversion because it’s counted as interest income for tax reporting purposes. Everyone has a different tax situation and should consult a tax advisor.

The IRA Match is treated as interest income in your IRA. We won’t deliver a 1099-INT due to the tax status of IRAs.